BME Clearing manages risk in a comprehensive manner, ensuring secure operations and compliance with EMIR regulations.

What Do We Offer?

BME Clearing acts as a central counterparty (CCP), intervening between the counterparties to a transaction to mitigate credit risk. Our mission is to guarantee the successful completion of transactions, providing security and stability to the market.

Contact Us

We will be happy to answer your questions.

Benefits

Detailed Operation

Default Waterfall Description

Content under review because of changes in BME Clearing 's Dedicated Own Resources due to the entry into force of articles 9.14 and 9.15 of the CPRRR last February 12 on the calculation of the Second Skin in the Game (SSITG). For more information, the documentation that has been updated for this reason can be found in the "Regulations" menu, as detailed below:

- BME Clearing’s Rulebook

- Circulars

- C-GEN-02/2023 Non-Default Losses Allowance for Investment Losses NDL.

- C-GEN-03/2023 BME Clearing Dedicated Own Resources (SITG) and Additional Dedicated Own Resources (SSITG).

The Circular ‘Dedicated Own Resources of BME Clearing’ is amended to provide greater clarity and to identify those related to the Skin in the Game (SITG) and those related to the Second Skin in the Game (SSITG).

- Circulars concerning the Default Fund of each Segment:

- C-DF-02/2023 Default Fund

- C-ENE-02/2023 Default Fund

- C-IRS-02/2023 Default Fund

- C-RV-03/2023 Default Fund

- C-VRF-03/2023 Default Fund

Solvency Requirements

One of the first lines of defense that BME Clearing has is to require a minimum level of equity to the entities in order to become a Member, depending on the Member category. This minimum level of equity is established in the General Conditions of each Segment.

Besides, BME Clearing may establish via Circular alternative Funds and requisites to those amounts of minimum equity level, which must provide with an equivalent level of solvency, availability and financial assurance, maintaining in any case a minimum equity level requirement of 20% the amounts indicated, for each type of Member.

In regard to Contracts belonging to each Segment, Members must provide BME Clearing with the information necessary for BME Clearing to meet, within the time frame and formats appropriate to each case, the reporting requirements of the CNMV or the Competent Authority, on the Transactions carried out in BME Clearing by these Members.

Margins

Skin in the Game

Content under review because of changes in BME Clearing's Dedicated Own Resources due to the entry into force of articles 9.14 and 9.15 of the CPRRR last February 12 on the calculation of the Second Skin in the Game (SSITG). For more information, the documentation that has been updated for this reason can be found in the "Regulations" menu, as detailed below:

- BME Clearing’s Rulebook

- Circulars

- C-GEN-02/2023Non-Default Losses Allowance for Investment Losses NDL.

- C-GEN-03/2023 BME Clearing Dedicated Own Resources (SITG) and Additional Dedicated Own Resources (SSITG).

The Circular ‘Dedicated Own Resources of BME Clearing’ is amended to provide greater clarity and to identify those related to the Skin in the Game (SITG) and those related to the Second Skin in the Game (SSITG).

- Circulars concerning the Default Fund of each Segment:

- C-DF-02/2023 Default Fund

- C-ENE-02/2023 Default Fund

- C-IRS-02/2023 Default Fund

- C-RV-03/2023 Default Fund

- C-VRF-03/2023 Default Fund

MEFFCOM2

BME Clearing has its own parametric model for Initial Margin calculation. It is called MEFFCOM2, which is similar to an SPAN model, quite an standard in the industry.

This model is used for Initial Margin calculation in the Financial Derivatives (for all contracts except xRolling FX), Cash Equities, Energy and Fixed Income Segments.

The model evaluates the worst possible loss of a portfolio considering several theoretical scenarios that can be increased by large positions (concentration risk).

The model allows offsetting risks bilaterally between different financial instruments (margin classes) as long as it has been verified the two instruments in question are sufficiently correlated (average correlation equal or greater than 70%).

In the case of the Cash Equities and Fixed Income Segments, MEFFCOM2 model has been adapted in order to deal with several position balances and several settlement scenarios (Intended Settlement Dates or ISDs).

For further detail about the Calculation of the Initial Margin using MEFFCOM2, please check our “Procedure for Margin Calculation" Circular of the relevant Segment.

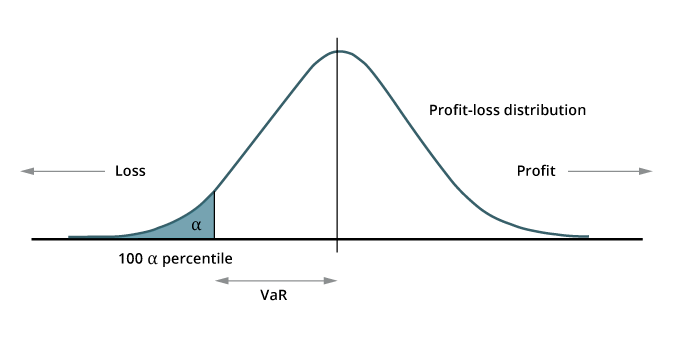

HVaR

Value-at-Risk (VaR) is a statistical measure that quantifies the maximum expected loss given a time horizon and assuming a confidence level.

In the case of the Swaps Segment and the xRolling FX contracts of the Financial Derivatives Segment, BME Clearing uses an Historical VaR model (HVaR) combined with Expected Shortfall (Tail VaR).

The HVaR uses historical data and scenarios.

The Expected Shortfall or Tail VaR is the expected value of the losses subject to being higher than a given level, in this case, the VaR. It would be the average of the losses within the tail of the distribution, that is to say superior to the VaR.

Between the advantages of using an HVaR model are:

- Greater capital efficiency (generates greater offsetting).

- Has greater accuracy by benefiting from a greater correlation and diversification effect.

- Greater robustness and greater flexibility, with the possibility to be applied to new products.

For further detail about the calculation of the Initial Margin using HVaR, please check our “Procedure for Margin Calculation" Circular of the relevant Segment.

Content under review because of changes in BME Clearing's Dedicated Own Resources due to the entry into force of articles 9.14 and 9.15 of the CPRRR last February 12 on the calculation of the Second Skin in the Game (SSITG). For more information, the documentation that has been updated for this reason can be found in the "Regulations" section:

BME Clearing has a document, Default Management Protocol.

BME Clearing offers different levels of segregation in compliance with EMIR. The structure of BME Clearing’s records and accounts, as regulated in its Rule Book, enable Members and Clients to hold different types of accounts.

Check here our Segregation and Portability Disclosure and our Account Structure offering.

The Central Counterparty, BME Clearing, puts itself before both counterparties in a financial transaction. When interposed, several risks affect the CCP. The main one would be the counterparty risk, also called credit risk. However, there are other risks that affect BME Clearing, amonge them concentration risk and the wrong way risk.