BME Clearing offers a comprehensive solution for clearing equity transactions, guaranteeing security, efficiency and transparency in the trading of shares, ETFs, warrants, rights and certificates. As a central counterparty, we eliminate counterparty risk and bring robustness to every stock market transaction.

What Do We Offer?

Contact Us

We will be happy to answer your questions.

Benefits

How Do We Operate?

Registration and automatic novation: Once the transaction reaches BME Clearing — via trading platforms or Iberclear — the rights and obligations towards our entity are automatically novated, making us the only counterparty for both parties.

Clearing through netting: We perform a net balance calculation, in which each participant is only responsible for their net position (buyer or seller), including the clearing house itself.

Sales withheld to guarantee settlement: If a client does not have securities to deliver, sales are withheld until the securities are in the account. Only then are they released for settlement, even applying limits to the net selling balance.

For more information, please refer to (link to the document or circular describing the operation).

Operation in Detail

The schedule about the procedures of BME Clearing Equity are:

|

Time

|

Process

|

|---|---|

|

00:00 (T-1) (*)

|

System connection.

|

|

Transfer of files. |

|

|

Start of the Hold / Release mechanism for trades with ISD T+1. |

|

|

Start of internal / external allocations and transfers. |

|

|

Reception of settlement information. |

|

|

08:00 |

End of release mechanism period with ISD T (day) for the first Intermediate Aggregation Window. |

|

Transfer of start of the first Intermediate Aggregation Window files. |

|

|

Settlement Instructions due to released trades are sent to IBERCLEAR. |

|

|

08:30 |

Transfer of end of the first Intermediate Aggregation Window files.

|

|

09:00 |

Start of reception of multilateral trades from the trading platform.

|

|

10:00 |

End of release mechanism period with ISD T (day) for the second Intermediate Aggregation Window.

|

|

Transfer of start of the second Intermediate Aggregation Window files. |

|

|

Settlement Instructions due to released trades are sent to IBERCLEAR. |

|

|

10:15 |

|

|

Transfer of end of the second Intermediate Aggregation Window files. |

|

|

12:00 |

End of release mechanism period with ISD T (day) for the third Intermediate Aggregation Window. |

|

Transfer of start of the third Intermediate Aggregation Window files. |

|

|

Settlement Instructions due to released trades are sent to IBERCLEAR. |

|

|

12:15 |

Transfer of end of the third Intermediate Aggregation Window files. |

|

14:00

|

End of release mechanism period with ISD T (day) for the fourth Intermediate Aggregation Window. |

|

Transfer of start of the quarter Intermediate Aggregation Window files.

|

|

|

Settlement Instructions due to released trades are sent to IBERCLEAR.

|

|

|

End of external allocation period for trades with TD = T-1 (previous day), except for SICAVs NAV. |

|

|

14:15 |

Transfer of end of the fourth Intermediate Aggregation Window files. |

|

15:30 |

End of release mechanism period with ISD T (day) for the last Intermediate aggregation window2. |

|

Transfer of start of the last Intermediate Aggregation Window files. |

|

|

Settlement Instructions due to released trades are sent to IBERCLEAR. |

|

|

PREA Instructions with ISD T (today) are sent to IBERCLEAR. |

|

|

16:00 |

End of DvP settlement period in real time. |

|

End of external allocation period for SICAV trades with TD = T-1 (previous day). |

|

|

End of internal allocations and transfers for trades with TD = T-1 (previous day). |

|

|

End of the reception of bilateral trades with ISD T+1 (next day). |

|

|

16:15 |

Transfer of end of the last Intermediate Aggregation Window files.

|

|

17:35 |

End of reception of multilateral trades from platforms. |

|

18:15 |

Registration of Corporate Actions from IBERCLEAR. |

|

19:00 |

End of the Hold / Release mechanism for trades with ISD = T+1 (next day).

|

|

End of the reception of corporate actions from the CCP. |

|

|

Registration of buy-in and cash settlement trades. |

|

|

Netting of trades3 with ISD T+1 (next day) - Night Cycle. |

|

|

Settlement Instructions are sent to IBERCLEAR. |

|

|

Transfer of netting trades files – Night cycle. |

|

|

20:00 |

End of the reception of Special trades from platforms. |

|

End of internal / external allocations and transfer for trades with TD = T (today).

|

|

|

End of the Hold / Release mechanism for trades with ISD <> T+1

|

|

|

23:45 (*) |

Transfer of EoD (End of day) files. |

(*) Las horas de inicio son orientativas. Dependerán del fin de procesos del día.

The account structure in BME Clearing is a set of three levels:

- Position account: where transactions and the resulting positions are booked. Registration can be either net or gross.

- Margin account: where required margins are registered.

- Collateral account: includes collateral posted (cash or securities) to cover the amount required in the margin accounts.

The combination of the 3 levels of accounts mentioned will form the so-called "Account Structure." The Account Structures available in the Equity Segment are as follows:

Proprietary: Structure that includes positions, margins and collateral of the Clearing Member or Segregated Non-Clearing Member.

Proprietary and Daily Position Accounts may form Proprietary Structures.

ISA: Structure that includes positions, margins and collateral of a single individual client. This structure, in turn, may be "Agency", where the owner of the structure is the client, or "Principal to Principal", where the owner of the structure is the Member.

Financial Intermediary and Individual position accounts may form ISA Structures.

OSA: Structure that includes positions, margins and collateral of several direct clients.

OSA structure may be used for Indirect Clearing, and will thus be called Indirect Clearing OSA available for indirect clients of the direct clients of members upon request.

Third party Position Accounts may form OSA Structures.

GOSA: Structure available for Indirect Clearing. The notion of this structure is very close to an OSA for indirect clients, which unlike the previous one, separates positions and the required margins from each indirect client that is part of the account. The required margin will be the result of adding the required margins in all margin accounts within the GOSA account. Lastly, the clients' collateral is registered in a single collateral account.

Indirect Clients Position Accounts for GOSAs may form GOSAs Structures.

The register of a transaction at BME Clearing involves the automatic novation of the buyer and seller rights and obligations. These are extinguished arising new rights and obligations with BME Clearing as the unique counterparty: buyer facing the seller and seller facing the buyer.

Trading platforms (or IBERCLEAR, when it acts as a platform) will send to BME Clearing the transactions that have been designated for novation.

Such designation can be:

- Global: all trades in the trading platform's electronic book (multilateral trades): Trading Members of the platforms introduce their orders in the Trading Platform and Trading Platform sends the executions to the BME Clearing in real time. The CCP validates each execution it receives and sends the transactions in real time to its Members.

- Trade by trade: a specific transaction designated as such by its’ counterparties. This is applicable to bilateral transactions.

Bilateral transactions from Block Trades will be registered in BME Clearing as well as bilateral transactions from Special Transactions if their counterparties decide so.

Bilateral trades will be received from IBERCLEAR. For this purpose, Settlement Participants act as Trading Members with a certain Member status in BME Clearing .

When novation is registered in a non-definitive Account, Members may allocate those trades.

When a member assigns operations between Position Accounts within its own account structure in BME Clearing, it will be considered Internal Allocation.

When a member wishes to transfer their operations to other Position Accounts of another CCP Member it will be considered External Allocation.

An Intra-Day Risk Limit (IRL) is assigned by BME Clearing to each Clearing Member. If a Clearing Member exceeds such Limit due to the impact of a price fluctuation in the current position or caused by novating new trades, it shall provide an Individual Fund to the CCP.

BME Clearing calculates the risk of each Account in real time.

In addition, at the end of the session, BME Clearing calculates the risk of the outstanding position pending to be settled at the end of day, for each Clearing Member. Margins to cover such risk are required to be posted next morning.

BME Clearing will demand from Clearing Member the following margins.

Initial Margin

Calculated daily for each outstanding position, for each account in BME Clearing Central Register, for each ISIN and Clearing Account (Proprietary Account and Individual Client Accounts). All transactions pending to be settled will be included taking into account a determined price fluctuation and determined compensations between correlated ISINs.

The positions pending to be settled include buy-and-sell transactions, failed positions and cash only positions.

Individual Fund

It may be requested for different reasons:

- Individual Fund for Risk Limits

- Individual Fund as a percentage of Daily Margin

- Individual Fund required to a Member which does not meet the minimum required Shareholders’ Equity.

- Individual Fund for Stress testing of the Default Fund.

- Voluntary Individual Fund.

Extraordinary Margins

Requested to hedge CCP risk in extraordinary cases.

Extraordinary Margins will be requested for:

- Situation of high volatility where Clearing Member exceeds the Extraordinary Margin parameters established by circular.

- Drop of the Member´s Solvency ratio below the level corresponding to the investment grade.

- Exceptional situation or high-risk situation of a Clearing Member.

Default Fund

Requested to cover any debit balances resulting from a Clearing Member default. BME Clearing, according with the Rule Book and Circulars, has a Default Fund separated by segment. In this way, if a Clearing Member does not have position or activity in a segment, a Clearing Member’s default due to losses in that segment can never affect him.

The minimum amount of the default fund is specified in the Default Fund Circular for each segment: 25 million euro for the Equity Segment.

This amount will be updated regularly and has a minimum contribution that changes depending on the Clearing Member’s typology.

The Settlement Participant may hold sales for which the client does not have enough securities to deliver, and release them when the securities become available in its Custody Account. Only then will these sale transactions be sent to the settlement process. The Settlement Participants will be in charge of managing this procedure since they know the securities available in the client’s Custody Accounts.

The Holding of Sales may be done during the day prior to the Intended Settlement Date of the transaction, and it will be executed transaction by transaction.

Only the selling net balance of the net position accounts in the BME Clearing will be eligible to be held. Thus, held sales will decrease the settlement instruction generated by BME Clearing as long as the net selling balance of the account allows it.

During ISD and as transactions are released by the Settlement Participant, BME Clearing will send Settlement Instructions for the aggregated of released transactions and its corresponding cash in each settlement window.

If at the end of the last aggregation window of the session a transaction has not been released, BME Clearing will aggregate all the held gross trades with ISD equals to the session, generating a single settlement instruction that will be sent to IBERCLEAR in PREA status.

Once the settlement instruction has been sent to IBERCLEAR, when the Participant Entity requests the total or partial release of the instruction to the CCP, BME Clearing will modify the status of the instruction to allow its settlement.

Netting or Aggregation and the consequent generation of Settlement Instruction (SI) will take place between 19:00 and 20:00 of the business day before to the Intended Settlement Date (ISD).

BME Clearing will perform netting or aggregation of position account’s transactions depending on the position account type:

- Transactions registered in gross position accounts will not be netted but rather will be gross settled (previous aggregation of transactions per ISIN and side).

- Transactions registered in net position accounts will be subject to netting if they have the following common attributes:

- Intended Settlement Date

- Trade Date

- ISIN

- Position Account

Failed Transactions from previous sessions and the sale Transactions from different dates held at BME Clearing are not involved in this process. Buy-in Transactions generated by BME Clearing in Fails Management are not netted either.

Once the CCP generates the Settlement Instructions, the original transactions stop existing and they are replaced in the CCP records by the Settlement Instructions. The entities are only responsible for compliance with the obligations of cash payment and securities delivery resulting from said Settlement Instructions.

Regarding to securities, the Netting will generate net buying, selling or null instructions. While, as regards cash, the netting will generate without or with payment instructions (receiving or delivering cash).

Settlement Instructions generated and sent to IBERCLEAR can be of the following types:

- Delivery versus payment

- Receive versus payment

- Delivery with payment

- Receive with payment

- Delivery free of payment

- Receive free of payment

- Payment free of delivery

- Collection free of delivery

- Payment instructions free of delivery and zero cash (are not sent to IBERCLEAR).

BME Clearing Equity send to T2S through IBERCLEAR before of the 20:00 the Settlement Instructions (SI) resulting of the Netting and Aggregation process, with Intended Settlement Date Next Business Day.

BME Clearing will be the counterparty to all Instructions using, for that purpose, its own cash and securities accounts in the Settlement System.

In case there are insufficient securities balance to settle a sell instruction, T2S, depending on its settlement algorithms, will establish which buying instruction will or will not be settled.

BME Clearing generates all SI that can be partially settled.

In the Settlement of Instruction process, priority is taken into account, it means, the order in which the Instructions are settled according to the T2S criteria. BME Clearing, as Central Counterparty, is assigned the TOP priority. In this way, all Settlement Instructions that the CCP sends to T2S, will have assigned this priority by default. Only the Central Bank or Central Securities Depositories will have higher priority.

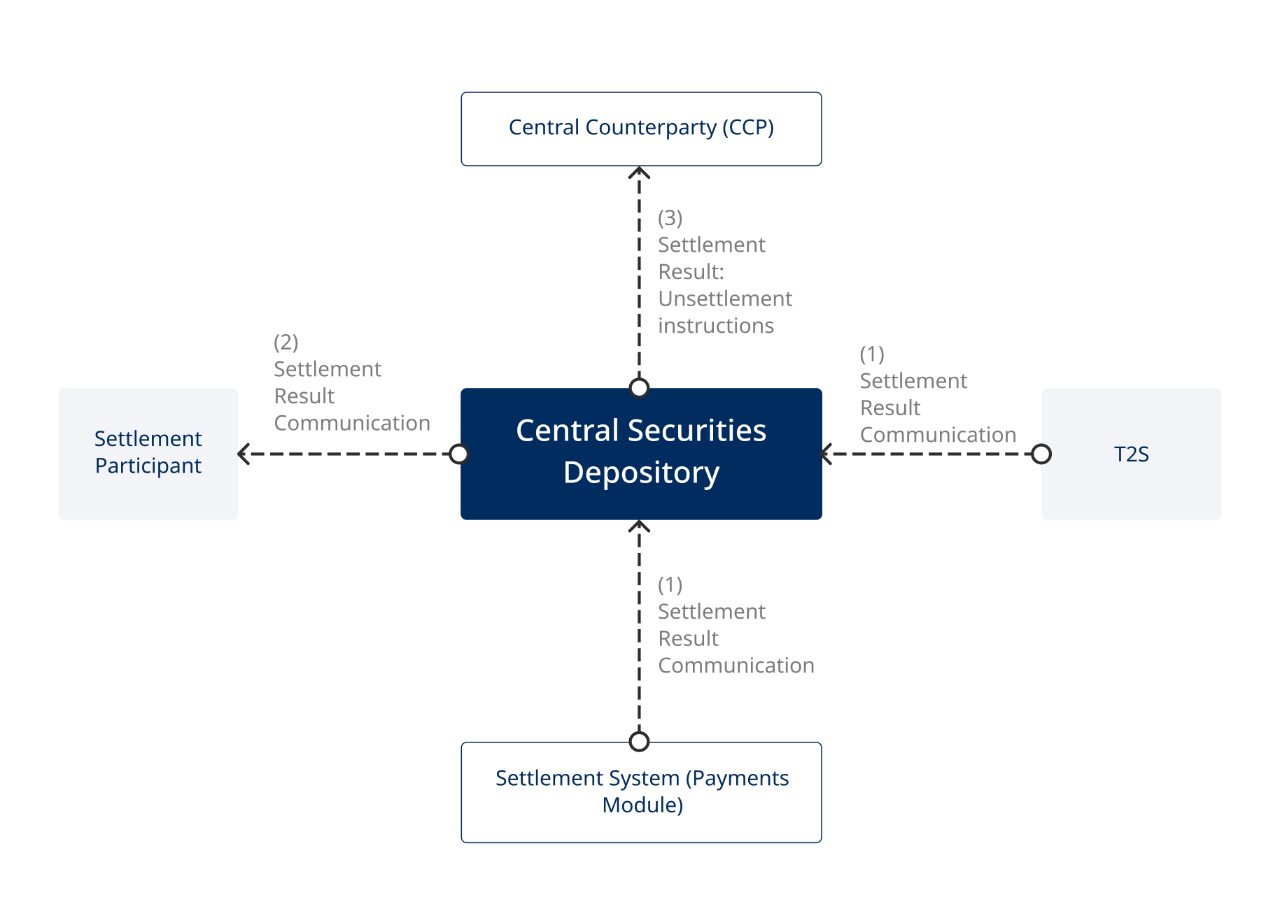

T2S will inform the CCP and the Settlement Participants about the status of the instructions when being settled and will also inform about the instruction status right after the settlement period. Unsettled instructions will remain in T2S for settlement in following sessions.

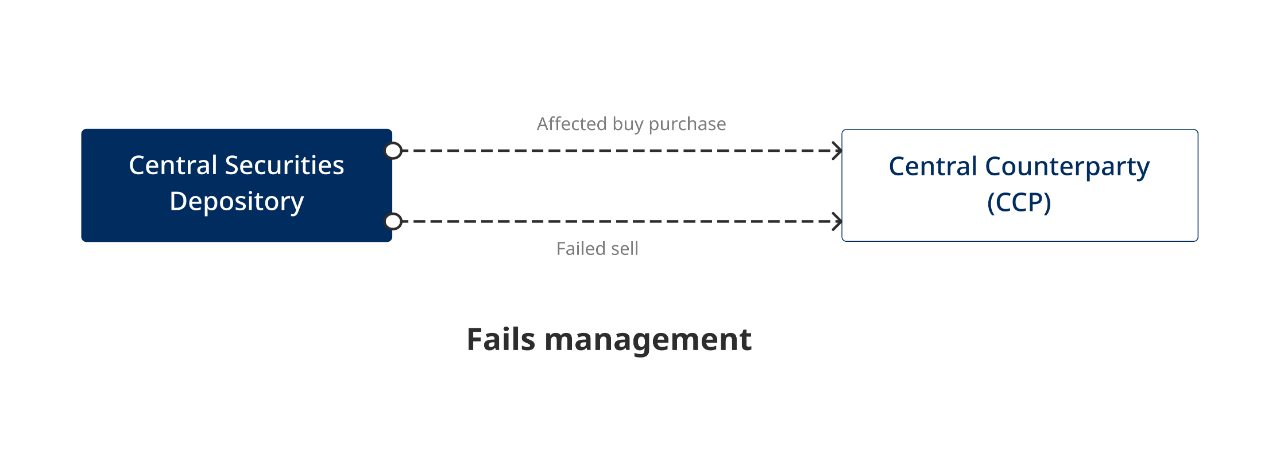

If a Settlement Instruction cannot be settled on its Intended Settlement Date (ISD), BME Clearing will initiate the Fails Management Mechanisms.

In this respect, a "fail" refers to a sell instruction that is pending settlement, either totally or partially, at the end of its ISD.

End of Intended Settlement Date (ISD)

BME Clearing receive from the Settlement System the information about the instructions that have not been settled on its ISD in T2S.

Subsequent Sessions Prior to the Start of Buy - In

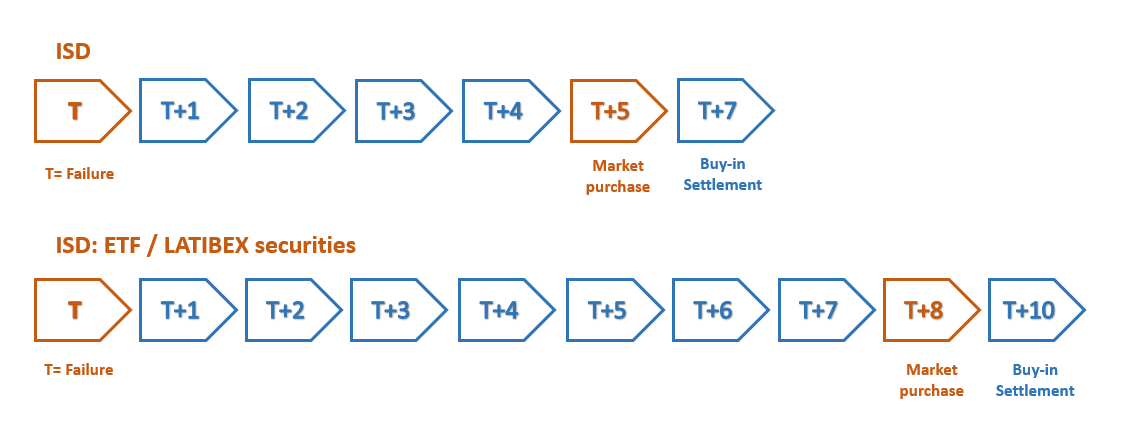

Any unsettled instruction will remain in recycling and will be attempted to be settled in subsequent sessions until ISD+5 (ISD+8 for ETF and LATIBEX securities).

If a failed sale instruction has not been settled by the end of ISD+5, it is held in the Settlement System and BME Clearing will iniciate the Buy-In procedure.

The deadline for initiating the buy-in procedure for ETFs and LATIBEX securities will be extended to ISD+8. If delivery of the securities is not possible, cash settlement will take place two days later.

Buy–in Procedure and its Settlement

Timeline for Buy-in procedure

BME Clearing will provide information on how many days late each failed position is.

At the end of the DVP settlement period, BME Clearing will hold the failed instructions that are on its ISD+5 (ISD+8 for ETF and LATIBEX securities).

A previously chosen broker will execute a purchase on the stock exchange for the amount not delivered by the failed member and once the broker´s purchase has been settled on ISD+7 (ISD+10 for ETF and LATIBEX securities), the securities will be delivered to BME CLEARING within a bilateral trade.

In ISD+7 (ISD+10 for ETF and LATIBEX securities) the CCP shall replace the failed seller's instruction with a new cash instruction for the difference between the cash from its initial failed transaction and the cash to be paid for the buy-in. All the instructions will settle during the ISD+8 (ISD+11 for ETF and LATIBEX securities) Night-Time Settlement Cycle.

The failed seller will cover the difference (if it is negative) between the cash position of the buy-in and that of the failed sale instruction, as well as the corresponding administrative costs.

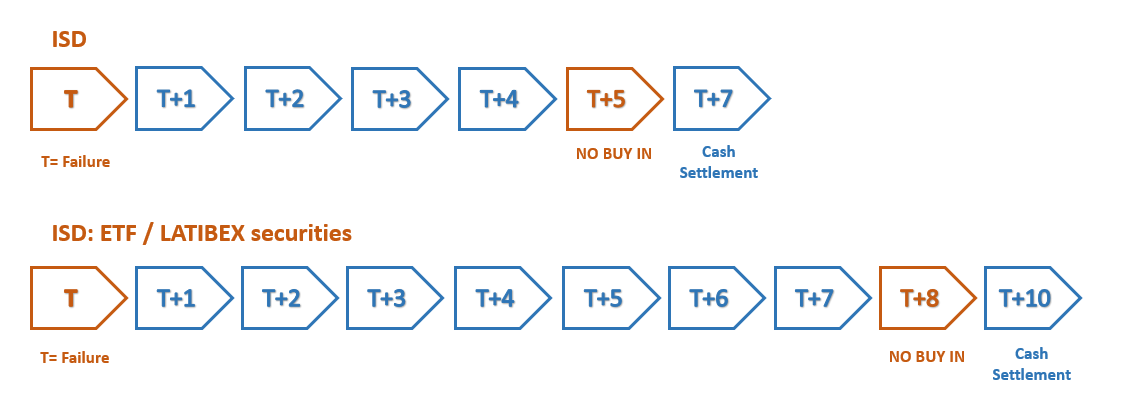

Cash Settlement

Cash Settlement Timeline

BME Clearing will perform Cash settlement if the buy-in is not executed due to the illiquidity of certain assets, or if the broker's purchase is not settled on ISD+7 (ISD+10 for ETF and LATIBEX securities).

Cash settlement will be performed on the next available settlement date to fulfil the outstanding obligations of the failed seller with the CCP and of the CCP with the affected buyer.

The affected buyer will be compensated with an amount of cash calculated using the last available closing price of the security, plus a percentage. The cash settlement price cannot be lower than the price of the failed sale or the affected buy that will be settled in cash.

Cash Settlement Price = Max (last closing price + %; price of the failed sell; price of the affected buy)

Rules on adjustments of transactions novated by the CCP are stablished by the CCP itself, but the Settlement System will generate adjustments in CCP instructions denominated in euro along with those carried out for failed transactions on Record Date (day on which the issuer determines which positions are to be taken into account for the calculation of the corporate event), that were not novated. The adjustments carried out by he Settlement System will be between the failed seller and the affected buyer.

It means, if a corporate action occurs and there are unsettled balances on Record Date, it is necessary to ensure that the benefit of the corporate event reaches the buyer of a failed transaction.

The Settlement System will manage corporate events over the instructions in euro sent for settlement by the CCP and which are pending settlement on Record Date.

The corporate event types, according to how they affect to the characteristics of the underlying security, are:

- Distribution: In these corporate actions, the characteristics of the underlying security is not modified. Cash or securities are distributed according to the position in the registry at the close of the Record Date. For example: payment of a dividend.

- Reorganization: In this type of corporate events the underlying security is modified. For example, reverse splits or capital increases.

Buyer Protection

The Buyer Protection functionality is a process whereby a buyer who has yet to receive the underlying securities of an Elective Corporate Action, to instructs the seller (CCP) in order to receive the outturn of his choice.

The Buyer Protection will be a manual mechanism by means of which the buyer can send a request to transform the instruction as per the option chosen. This occurs when, on the last day the security that is entitled can be settled, there are instructions that remain unsettled. This application must be delivered by the buyer’s Settlement Participant to BME Clearing before the Buyer Protection Deadline, a date determined in the Corporate Action as the last moment for receiving Buyer Protection instructions.

Penalties

According to the amendment of Article 19 of the Delegated Regulation (EU) 2018/1229 on Settlement Discipline Regime (‘SDR’), regarding the penalty mechanism for settlement failures of cleared transactions, which came into effect on September 2, 2024, the Central Securities Depository (‘CSD’) will be responsible for calculating and managing the collection and distribution of penalties to be applied to non-compliant entities.

BME CLEARING will not make any communication or management in this regard.

Administrative Costs

Administrative costs for the failed seller

A penalty of €50 per day is applied to the failed seller for each failed instruction that remains failed once its ISD has been reached.

Administrative costs for buy – in and/or cash settlement

A penalty of 1 bps plus a fixed administrative cost of €1,.000 for each Failed Settlement Instruction to which a buy-in process is executed (without taking into account the number of attempts or buy-ins), or for each cash settlement.

Members and entities may use any of the available options to communicate with the CCP and receive information, through messages and/or files.

The specifications are available in the private area of the BME CLEARING website.

Files

Reporting frequency

The activity of each Member will be informed by BME Clearing through detailed files as below:

- Start of Day (SoD), once BME Clearing opens its activity for the corresponding session.

- Intradía (ID), the settlement files are generated in different temporary Windows during the day.

- End of Day (EoD), once BME Clearing close its activity for the corresponding session.

Ways of obtaining files

Obtaining the files will be through access to SFTP server of BME Clearing . Alternatively, queries can be made to the GUI that is made available to Members (BME PC), which contain the same information as the files.

Messaging

Igualmente la actividad de cada Miembro será informada por BME CLEARING a través de mensajería online en tiempo real, en los siguientes protocolos: FIXML, Propietario o ISO.

Equity is the segment through which the Central Counterparty (CCP) of BME provides clearing and CCP services for the trading of securities listed on its equity markets, specifically shares, rights, warrants, certificates and exchange-traded funds (ETFs).

To this end, BME Clearing stands between a buyer and a seller in the market, thus becoming the counterparty to each trading party.

Prior to issuing the settlement instructions a process called netting (the clearing of net balances) takes place, in such a way that the only obligations to be honoured by each participant in the CCP as well as by the CCP itself are those arising from their net positions.

The main advantages of the segment are that it allows customers to benefit from capital consumption efficiencies by using a CCP instead of taking on counterparty risk, which entails higher capital consumption and risk. In addition, thanks to the regulatory mechanisms providing the CCP with solid legal protection, the CCP contributes to greater market stability by mitigating counterparty and operational risk and ensuring the finality of trades.

The CCP also helps optimise the management of guarantees in such a way as to minimise the impact on participants of compliance failures.

Frequently asked questions

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Vivamus at auctor mauris. Nullam feugiat tempor neque, sed dignissim massa accumsan eget. Duis mauris magna, eleifend a mauris in, sagittis viverra felis. Curabitur ornare malesuada accumsan. Suspendisse sollicitudin diam nec pretium mattis. Proin porta lacus vel sem venenatis, ut egestas nunc maximus. Curabitur rutrum nibh pharetra enim faucibus mattis. Phasellus malesuada ligula non purus fringilla, quis sollicitudin sem tincidunt. Vestibulum lacus est, consequat ut risus vitae, tincidunt posuere nisi. Praesent nibh lacus, ullamcorper eget auctor vel, mattis at mauris. Proin sed elit justo. Nunc tempus sapien velit, at feugiat nisi bibendum eu. In at bibendum nisl, non posuere mi. Fusce tincidunt, ligula a consectetur sagittis, velit est feugiat nulla, eu vehicula sapien magna ut nunc.