BME Clearing offers a robust solution for the clearing of European sovereign debt transactions, providing security, efficiency and traceability in risk management.

What Do We Offer?

Types of Debt Cleared

Sovereign bonds and debentures: with fixed, floating or inflation-indexed coupons.

Treasury bills: from Spain, Italy, Portugal, France, Germany, Austria and the Netherlands.

Types of Transactions Accepted

Simultaneous: purchase and sale transactions with simultaneous settlement.

Classic repos: repurchase agreements with delivery of securities and cash.

Operations

- Registration and novation: Trades are automatically registered and novated, becoming contracts with BME Clearing as the central counterparty.

- Margin calculation: Margin requirements are calculated in real time, requiring collateral deposits according to the risk of each member.

- Generation of settlement instructions: BME Clearing generates and sends settlement instructions to Iberclear/T2S for execution.

- Settlement and management of fails: Settlements are managed and possible failed positions are addressed, ensuring compliance with obligations.

Contact Us

We will be happy to answer your questions.

Benefits

Detailed Operation

The schedule about the procedures of BME CLEARING Fixed Income are:

|

Time

|

Process

|

|---|---|

|

00:00 (T-1) (*) |

Connecting systems.

|

|

Delivery of files. |

|

|

Receipt of settlement information. |

|

|

From 8:00 to 15:50

|

Registration of bilateral transactions with Intended Settlement Date on the same day (T). |

|

Settlement Instructions with ISD = T are sent to IBERCLEAR.

|

|

|

From 8:00 to 18:20

|

Registration of bilateral transactions with Intended Settlement Date different to T. |

|

8:00, 8:15, 10:00, 10:15, 12:00, 12:00, 12:15, 14:00, 14:15, 15:45, 16:15

|

Delivery of files. |

|

From 18:00 to 19:00

|

Corporate Events adjustments originated by IBERCLEAR. |

|

From 19:00 to 20:00

|

Netting of transactions with ISD T+1 (next day) - Night Cycle. |

|

Settlement Instructions are sent to IBERCLEAR. |

|

|

Transfer of netting transactions files - Night Cycles. |

|

|

From 23:30 to 00:30 |

Transfer of End of Day (EoD) files.

|

(*) Starting times are approximate. They will depend on the end of the day processes.

The registration of a transaction in BME Clearing Fixed Income entails the automatic novation of the rights and obligations of the buyer and seller. These are extinguished, giving rise to new rights and obligations with BME Clearing as the unique counterparty: buyer facing the seller and seller facing the buyer.This way, greater efficiency is achieved in settlements through netting and control of securities and cash delivery process.

Transactions subject to registration are buy/sell-back transactions and classic repos in Spanish, Italian, Portuguese, French, German, Austrian and Dutch debt. Market standard assumes buy/sell back for Spanish Debt and classic repo for European debts, however, members can specify trades different from the market standards.

Underlying Securities of the accepted transactions admitted for registration are:

- Sovereign Bonds and Obligations with fixed and variable coupon and indexed to inflation.

- Treasury Notes.

Debt Strips and transaction terms that exceed 36 months are not accepted.

BME Clearing is authorized to register simple transactions and double, buy/sell-backs or classic repos.

The transactions can be received from SENAF and BrokerTec Platforms and those admited to be settled in IBERCLEAR acting as Platform. In addition, BME Clearing allows direct registration through the CCP.

In the Central Register and for the Fixed Income Segment different types of Clearing Accounts can be opened:

- Proprietary Account (PA), whose holder is the CCP Member, in which the Member´s proprietary transactions are registered.

- Segregated Account (ISA), whose holder can be any natural or legal person and where Client Position is displayed at any moment.

- Omnibus Segregated Account (OSA), with positions of several clients whose holder is a Member, which may be in gross or net registration.

Proprietary Account can only target a Proprietary Account or an Individual Account at IBERCLEAR, while the Individual Segregated Account may also target a Third-Party Account at IBERCLEAR. Omnibus Segregated Accounts can only be addressed to a Third-Party Account at IBERCLEAR.

The opening of BME Clearing Fixed Income clearing accounts aimed at a Third-Party Account at Iberclear is condicioned on a prior request from the interested Member.

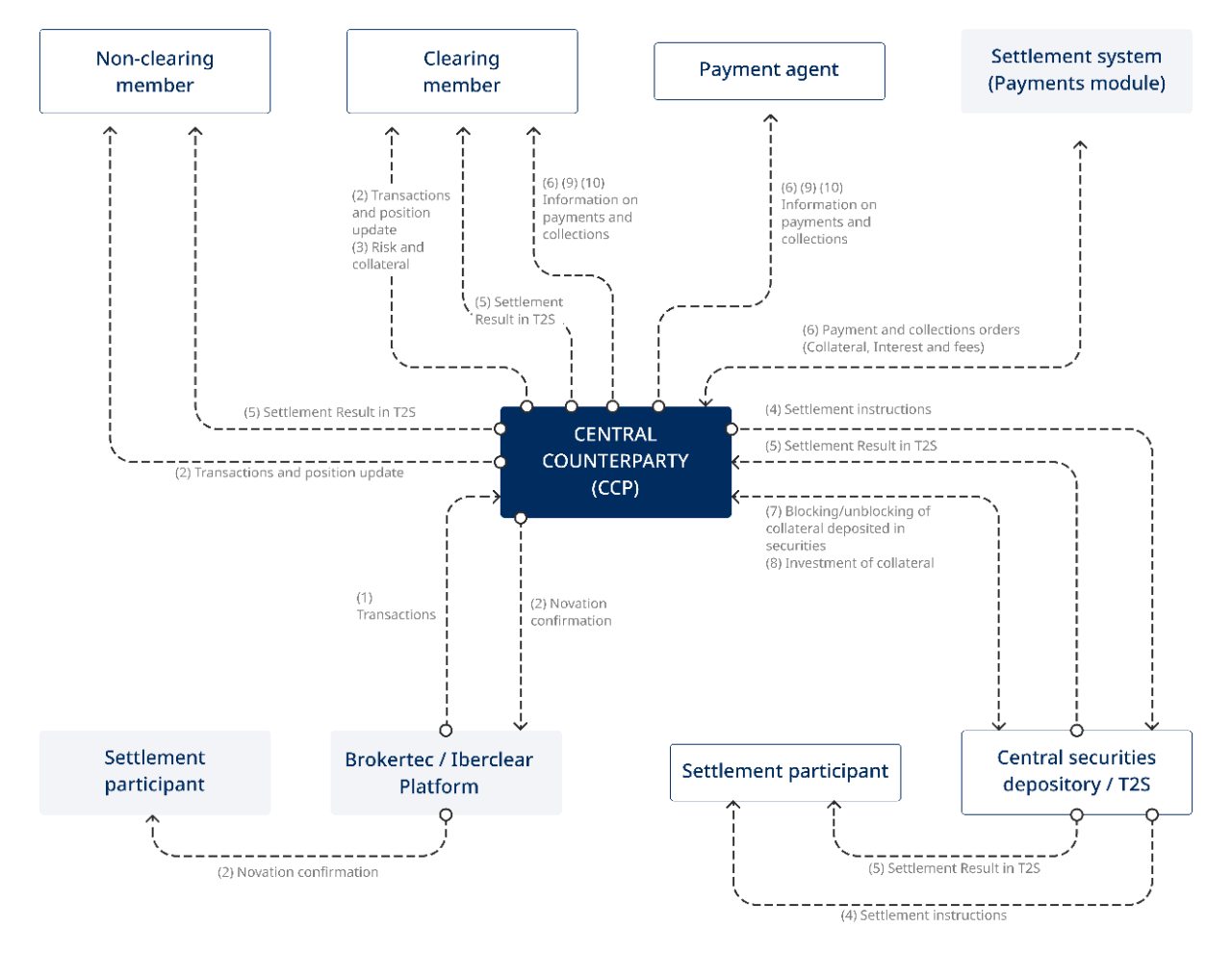

The communication and exchange of information between the different participants involved in the registry of transactions at BME Clearing Fixed Income is shown in the following table:

(1) The Central Counterparty (CCP) will receive in real time information on transactions that the member intends to novate coming from IBERCLEAR or SENAF and BrokerTec platforms.

(2) The CCP will confirm the novation of all trades to the Platform.

(3) The CCP calculates the risk of each account in real time. In addition, at the end of the session, the CCP calculates the risk of the outstanding position pending to be settled, for each Clearing Member. Margins to cover such risk are required to be posted next morning.

(4) The CCP generates the Settlement Instructions and sends them to T2S through the CSD (IBERCLEAR); then the CSD sends it to its Settlement Participants.

(5) The CCP will provide its Members, and IBERCLEAR its Settlement Participants, the result of the settlement and the CCP will manage the fails that may occur.

(6) Debit and credit orders for cash collateral.

(7) Blocking/ unblocking of securities collateral.

(8) Cash investment through buy/sell-back transactions.

(9) If applicable, interests payments resulting from investment.

(10) Debit and credit orders for other concepts of cash movements, i.e. payment of fees, penalties for fails, etc.

BME Clearing Fixed Income monitors position and risk, previous to the registration of each buy-sell transaction.

The registration of a new buy/sell back transaction or repo in a given ISIN, in BME Clearing Fixed Income will be conditioned on not exceeding the Position Limit. This Limit depends on the ISIN residual maturity tranche, on the net position previously registered in that tranche and on the Market Average Daily Volume per tranche.

At the same time, an Intra-Day Risk Limit (IRL) is assigned by BME Clearing to each Clearing Member. If a Clearing Member exceeds such IRL due to the impact of price fluctuation in the current position or attempts to novate new trades, they must make a contribution to the CCP in the form of an Individual Fund.

BME Clearing calculates the risk of each Account in real time. Furthermore, at the end of each session, BME Clearing calculates the risk of each Clearing Member for the outstanding position pending settlement, requiring that the deposit of margins to cover such risk are posted the next morning.

Specifically, BME Clearing will require Clearing Members o provide margins as below:

Initial Margin

Calculated daily for each outstanding position, for each open account in the CCP Central Register, for each ISIN and Clearing Account (Proprietary Account and Individual Segregated Accounts). All transactions pending settlement will be computed, taking into account a certain price fluctuation and compensation between different correlated ISINs.

The outstading positions pending settlement include buy-sell transactions, failed positions and cash-only positions. On the other hand, the balances of buy-sell positions to be considered for risk calculation correspond, to the net balance of purchases and sales pending settlement.

Extraordinary Margins

Requested to hedge CCP risk in extraordinary cases.

Extraordinary Margins will be requested for:

- Situation of high volatility where Clearing Member exceeds the Extraordinary Margin parameters.

- Drop of the Member´s solvency ratio below the investment grade level.

- Exceptional or high-risk situation of a Clearing Member.

Default Fund

According to the Rule Book and Circulars, BME Clearing has a separate Default Fund by segment. Thus, if a Clearing Member does not have position or activity in a segment, a default by a Clearing Member due to losses in that segment can never affect them.

The minimum amount of the Default Fund is specified in the Default Fund Circular for each segment: 25 million euros for the Fixed Income segment.

It is updated monthly and has a minimum amount that varies according to the risk and typology of the Clearing Member.

Individual Fund

It may be requested for different reasons:

- Individual Fund for Risk Limits.

- Minimum Individual Fund for the Fixed Income segment.

- Individual Fund for not reaching the required minimum Own Resources.

- Individual Fund for Stress Test of the Default Fund.

- Voluntary Individual Fund

Generation of Settlement Instructions

Netting, Aggregation and generation of Settlement Instructions (SIs) will take place between 19:00 and 20:00 of the business day before to the Intended Settlement Date (ISD).

Regardless of the position account´s type in which the Settlement Instructions are registered, SIs that correspond to the initial transactions, or the initial leg, of the buy/sell-back or repo transactions registered on their ISD, will be sent to be settled in real-time individually and in gross amount.

BME Clearing will implement Netting or Aggregation of registered transactions into the same position account based on the type of position account, differentiating between Net Position Accounts and Gross Position Accounts:

- Transactions registered in gross position accounts will not be netted but rather will be settled gross (after aggregation of transaction by directionand ISIN).

- Transactions registered in net position accounts will be subject to netting if they have the following common attributes:

- Intended Settlement Date.

- ISIN.

- Position Account.

Failed transactions pending settlement from previous sessions are not part of the netting process and will be treated gross. Buy-in transactions generated by BME Clearing in Incident Management in settlement are not netted either and will also be treated gross.

Once BME Clearing generates the Settlement Instructions, the original transactions are cancelled and replaced in the BME Clearing’s records by the Settlement Instructions. Entities are only responsible for fulfilling the cash payment and securities delivery obligations resulting from these Settlement Instructions.

Regarding securities, netting will generate net buying, selling or null instructions. While, regarding cash, netting will result in instructions without payment or with payment (receiving or delivering cash).

Settlement Instructions generated and sent to Iberclear can be of the following types:

Delivery versus payment.

Receipt versus payment.

Delivery with payment.

Receipt with payment.

Delivery free of payment.

Receipt free of payment.

Payment without delivery of securities.

Collection without delivery of securities.

Payment instructions without delivery of securities with zero cash (not sent to IBERCLEAR).

BME Clearing Fixed Income sends the Settlement Instructions (SIs) to T2S through IBERCLEAR to be settled with value date T (same day) in real time, and before 20:00 the resulting instructions of the Netting and Aggregation process, with Intended Settlement Date T+1 (Next Business Day).

BME Clearing will act as the counterparty of all Instructions, meaning it will intervene in every settlement, using for that purpose, its own securities and cash accounts in IBERCLEAR/T2S.

In case there are insufficient securities balance to settle a selling instruction, T2S, according to its settlement algorithms, determines which buying instruction will or will not be settled.

BME Clearing generates all SIs so that they can be partially settled. The parameters for the partial settlement are those in the static data in T2S for Fixed Income:

- Minimum unit of 100,000 euros in cash.

- Multiple settlement of 1,000 euros in notional.

In the Settlement of Instruction process, priority is taken into account, that is, the order in which the Instructions are settled according to the T2S criteria. BME Clearing as a Central Counterparty by the mere fact of being one is assigned the TOP priority. Thus, all Settlement Instructions sent by the CCP to T2S, will have this priority assigned by default. Only Central Banks or Central Securities Depositories will have higher priority.

T2S will inform the CCP and the Settlement Participants about the status of the instructions being settled, and will also inform about the status of the instructions at the end of each settlement period. Unsettled instructions will remain in T2S for settlement in the next settlement period or cycle.

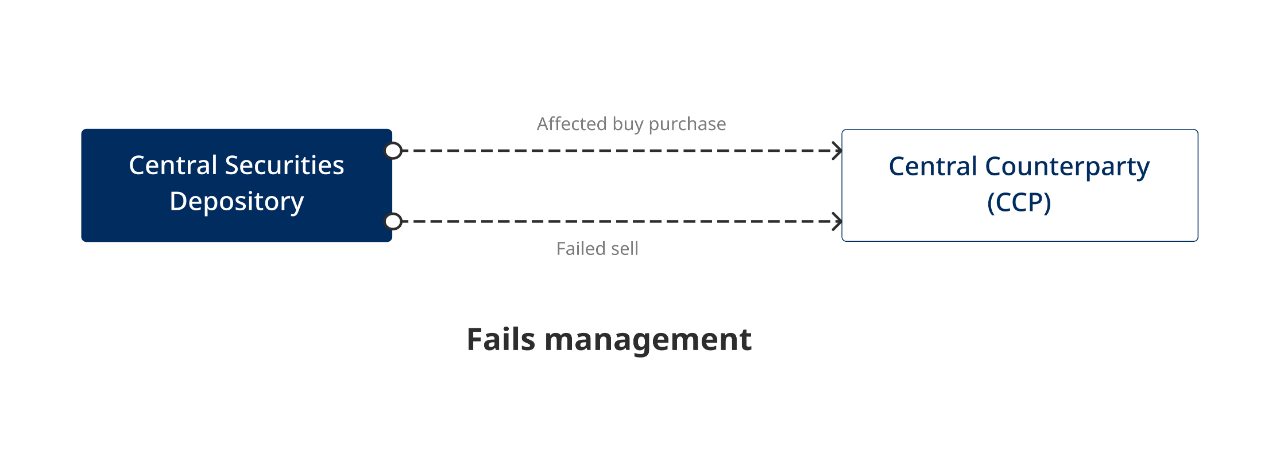

When a Settlement Instruction cannot be settled in its Intended Settlement Date (ISD), BME Clearing will initiate the Fails Management Mechanisms.

In this respect, a Fail is a sell instruction that remains pending settlement, either totally or partially, at the end of its Intended Settlement Date (ISD).

At the End of Intended Settlement Date (ISD)

BME Clearing receives from IBERCLEAR the information about the instructions that have not been settled in its ISD in T2S.

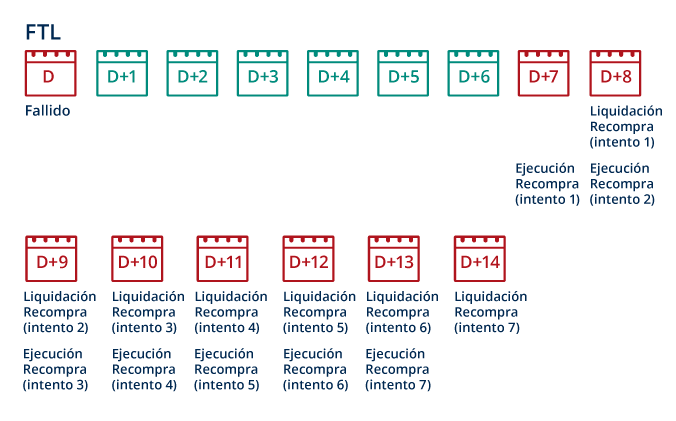

Subsequent Sessions Prior to the Start of Buy-in

Unsettled instructions will remain in recycling and attempts will be made to settle them in the following sessions until ISD+7.

If a failed sell instruction has not been settled at the end of ISD+7, it is held in the system and BME Clearing will begin the buy-in process by informing the market about the securities that will be subject to buy-in and the tender price (maximum bid price). Potential providers of securities will submit their offers.

BME Clearing will notify the selected securities provider that they have been selected and the provider will commit to delivering the securities to the CCP one day later, in ISD+8, in the CCP’s Settlement Account in T2S.

Buy-in and Settlement Procedure

If all the securities to be repurchased are not obtained on the first attempt, BME Clearing carries out more buy-in attempts in the following days (up to a maximum of 7 days) until all the securities are obtained:

Buy-in temporary schema

Cash Settlement

When performing the buy-in in ISD+7 is not possible (in case of the maturity of the security) or when the operation remains failed at the end of ISD+13, a cash settlement will be performed with the following day value to settle the outstanding obligations of the failed seller with the CCP and the CCP with the affected buyer.

The affected buyer will be compensated with an amount of cash calculated by the cash settlement price, and it will be performing through a cash amount equal to:

Cash settlement Price x Nominal – SI cash f the affected buyer to be settled in cash.

Cash settlement Price = Max (latest closing SENAF Price* 2% + accrued interest in T+1; Price of the failed sale; Price of the affected purchase).

Rules on adjustments of buy/sell-back transactions novated by BME Clearing are stablished by the CCP itself, but the Settlement System will generate adjustments for BME Clearing instructions along with those carried out for failed transactions on Record Date (the day on which the issuer determines which positions are to be taken into account for the calculation of the corporate event) that were not novated. The adjustments carried out by the Settlement System will be between the failed seller and the affected buyer.

That is, if a corporate event occurs and there are unsettled balances on Record Date, it is necessary to deliver the benefit of the corporate event to the buyer affected by a failed sale.

For repo transactions with an intermediate coupon payment, BME Clearing will make a settlement process on the value date of the coupon payment, through TARGET2, to charge the coupon amount to the holder of the securities at that time, and credit it to the original owner.

The corporate event types, depending on how they affect to the characteristics of the underlying security, are:

- Distribution Events: In these corporate events, the characteristics of the underlying security is not modified. Cash or securities are distributed according to the position in the registry at the close of the Record Date. For example: in BME Clearing Fixed Income segment, it is the coupon payment.

- Reorganization Events: In this type of corporate events, the underlying value of the security is modified. For example: in BME Clearing Fixed Income segment, it is the final redemption.

Penalties

In accordance with the amendment of Article 19 of the Delegated Regulation (EU) 2018/1229 on Settlement Discipline Regime (‘SDR’), regarding the penalty mechanism for settlement failures of cleared transactions submitted by CCPs for settlement, effective September 2, 2024, the Central Securities Depository (‘CSD’) will be responsible for calculating and managing the collection and distribution of penalties to be applied non-compliant entities.

BME CLEARING will not make any action or management in this regard.

Administrative Costs

Administrative costs for the failing seller

A penalty of €50 per day will be applied to the failing seller for each failed instruction once its ISD is reached.

Administrative cost for buy in and/or cash settlement

A penalty of 1 bps plus a fixed administrative cost of €1.000 for each Failed Settlement Instruction to which buy-in process is executed (regardless of the number of attempts or buy-ins), or cash settlement.

Members and entities may use any of the available options to communicate with BME Clearing and receive information, through messages and/or files.

The specifications are available in the private area of the BME Clearing website.

Files Reporting Frequency

The activity of each Clearing Member will be reported by BME Clearing through detailed files twice a day, as described below:

- Intraday (ID), settlement files are generated in different time windows throughout the day.

- End of day (EoD), once BME Clearing has closed its activity for the corresponding session, it will send the files.

Ways of Obtaining Files

The files at the end of the session will be obtained through access to BME Clearing SFTP server. Alternatively, queries can be made to the GUI that is made available to Members (BME PC), which contain the same information as the files.

BME Clearing Fixed Income is the denomination for the Fixed Income Segment of the Central Counterparty (CCP).

Participants of BME Fixed Income may be all entities that wish to be Clearing Members or those that wish to be Clients of a Clearing Member under an account within the latter.

BME Clearing acts as a Central Counterparty (CCP) for transaction of Fixed Income Securities traded on stock exchanges, electronic trading systems or OTC between Clearing Members and/or Clients. Nowadays, BME Clearing Fixed Income cleared transactions are buy/sell-back or repo transactions on Spanish, Italian, Portuguese, French, German, Austrian and Dutch Sovereign Debt.

BME Clearing receives in real time information of transactions that members intend to novate and confirms the novation of the transaction to the corresponding Platform, updating the Member´s position in the corresponding CCP account. BME Clearing generates the settlement instructions.

Likewise, both in real time and at the end of each session, BME Clearing calculates the risk of each Clearing Member for the outstanding position pending to be settled requiring margins to cover it and informing the entities involved. Members are also provided with the result of the settlement managing any position defaultsf that may occur.

Buy In

No hay datos para el día de hoy

Frequently asked questions

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Vivamus at auctor mauris. Nullam feugiat tempor neque, sed dignissim massa accumsan eget. Duis mauris magna, eleifend a mauris in, sagittis viverra felis. Curabitur ornare malesuada accumsan. Suspendisse sollicitudin diam nec pretium mattis. Proin porta lacus vel sem venenatis, ut egestas nunc maximus. Curabitur rutrum nibh pharetra enim faucibus mattis. Phasellus malesuada ligula non purus fringilla, quis sollicitudin sem tincidunt. Vestibulum lacus est, consequat ut risus vitae, tincidunt posuere nisi. Praesent nibh lacus, ullamcorper eget auctor vel, mattis at mauris. Proin sed elit justo. Nunc tempus sapien velit, at feugiat nisi bibendum eu. In at bibendum nisl, non posuere mi. Fusce tincidunt, ligula a consectetur sagittis, velit est feugiat nulla, eu vehicula sapien magna ut nunc.