BME Clearing offers a robust platform for centralized clearing of OTC derivatives, specializing in interest rate swaps (IRS), forward rate agreements (FRA) and overnight index swaps (OIS). Our service guarantees legal certainty, operational efficiency and counterparty risk reduction, establishing us as the European alternative for managing your IRS.

What Do We Offer?

Contact Us

We will be happy to answer your questions.

Benefits

How Do We Operate?

Registration and novation

- Once the transaction is confirmed, automatic novation occurs, replacing the original counterparties with BME Clearing as the central counterparty.

Clearing and netting

We calculate net positions, reducing exposure and regulatory capital required.

We support various types of euro-denominated swaps with international standards (IRS, FRA, OIS).

Collateral and margins

We require initial margins and daily variation, adapted to EMIR regulations and international risk management standards.

Settlement

- Net cash payments from swaps are made, with clear and predictable processes that optimize cash flow.

Clearing and Settlement

Once the trade is registered it creates an open position. The open position can be managed via the Post-Record events detailed in the corresponding section.

Open transactions will be identified through the open-close indicator:

|

Indicator

|

Description

|

|---|---|

|

"O" |

Open

|

|

"C"

|

Close

|

Para identificar el tipo de operación que el miembro podrá realizar cualquiera de las siguientes acciones para gestionar correctamente su posición.

|

Indicador

|

Descripción

|

Detalle |

|---|---|---|

|

"B"

|

Backloading

|

Operación que se acepta en la Cámara días después de que se haya acordado. |

|

"F" |

Subasta |

Operaciones que provienen del proceso de gestión de incumplimiento. |

|

"H" |

Aplicación/Registro de la operación |

Aceptación de la operación en Cámara. |

|

"N" |

Neteo |

Operaciones que tienen perfiles económicos idénticos se comprimen en una sola posición. |

|

"T" |

Traspaso de operación |

Traspaso de una operación de un miembro a otro Miembro. |

|

"V" |

Vencimiento de contrato |

Operación de IRS que llega a su vencimiento. |

|

"Z" |

Traspaso de posición |

Traspaso de la posición de un miembro a otro Miembro. |

Daily settlements are made using a standard multilateral settlement in the Bank of Spain TARGET-2 system.

The clearing member requires an account in the TARGET-2 payments module. If it does not have one it may designate a payment agent who has a treasury account in a central bank of the euro system so that it can make settlements through it.

All intraday margins received by the CCP, either individual or extraordinary, made via a payment transfer or a direct debit, are also paid into the CCP’s account in the TARGET-2 Banco de España platform.

Additional settlements which apply to the IRS segment are described below:

Profit and loss daily Settlement

During the life of an IRS until the maturity day, a daily settlement of profit and losses for the variation of the NPV of the portfolio of a Clearing Member occurs due to fluctuations in the zero coupon since its last revaluation by BME CLEARING.

Price Alignment Interest (PAI)

It is the amount of accrued interest on the accumulated VM. It is a payment or charge to offset the imbalance between bilateral contracts and an IRS in CCP.

Coupons

Payment of fixed or floating coupons of registered transactions will be the result adding up the coupons to be received, less the coupons to pay with the same effective payment date, as set out in the Circular “Clearing Timetable and Procedure".

Additional Payments (Considerations)

Refers to additional payments of registered transactions, settlement will be done by adding up additional payments to be received and subtracting the additional payments to be made with the same cash payment date.

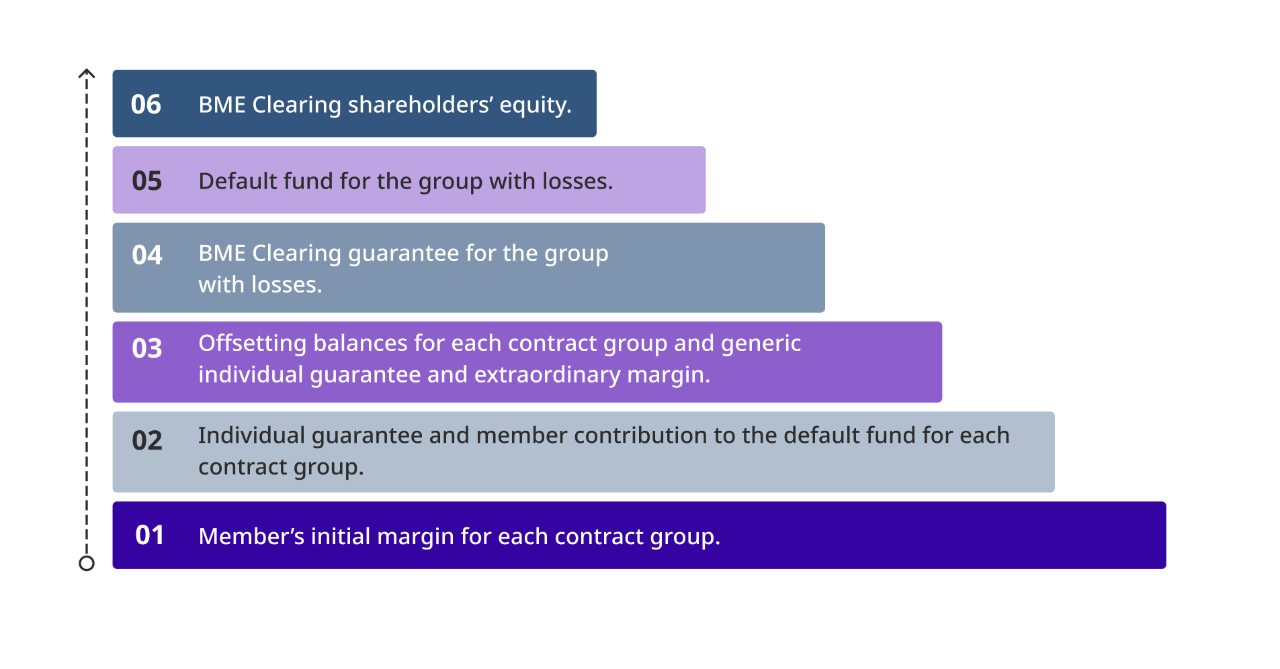

BME CLEARING SWAPS in order to cover for possible potential losses to which it is exposed under the IRS segment, requires the following margins from its Clearing Members:

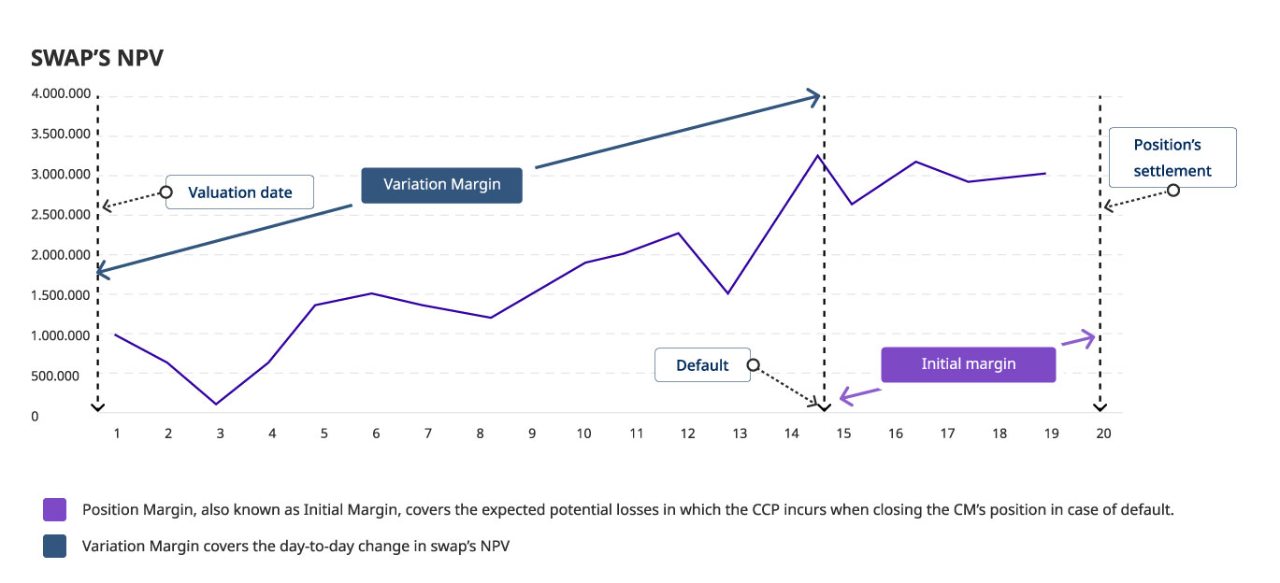

Initial Margin

It represents the potential loss of value that could be due to variation in interest rates during the five days deemed necessary to liquidate the positions in case of default. It is calculated at the account level.

This margin covers the risk of loss during the process of liquidating the Clearing Member's own position and their clients in case of default.

Variation Margin

It represents the portfolio's unrealised gain or loss. Is the daily sum of the Net Present Value (NPV) of the positions.

Individual Fund

This is only requested to Clearing Members. It consists of various items depending on the type of member and its solvency, consumption of limit risk and extraordinary situations arising (in this case the margin is called extraordinary margin). This type of margin only covers obligations from the Clearing Member, and can never be used to cover another Member’s default.

Default Fund

This is a joint liability guarantee. It will be used only to cover the default of another learing member in case all other margins from the clearing member plus the BME Clearing´s margins are not sufficient to cover the obligation.

On a monthly basis, BME Clearing will do a stress test, comparing the risk in stress test situations for each clearing member within the IRS segment default fund. In accordance with the corresponding Circular an additional individual margin will be requested to the Clearing Member, if necessary.

BME Clearing Guarantee

Margin posted by the Clearing House, greater or equal to the biggest contribution to the default fund by any clearing member in the IRS Segment. The amount is set by Circular.

Default Management

BME Clearing objective is to protect members and clients' positions. In addition to the margin schema set by BME Clearing, a procedure has been developed to protect the CCP and its clearing members and clients' positions if a Clearing Member enters in default.

In case a Clearing Member (CM) fails to comply with its obligations described in the Rule Book and the relevant circulars, BME Clearing SWAPS may declare such CM in default. With this declaration begins the Default Management Process (DMP), which comprises the following steps:

- Constitution of the Default Management Group, which advises the CCP at any time of the default process.

- Portability of positions of the Defaulting Clearing Member’s (DCM) Clients accounts to another non-defaulting Clearing Member (NDCM) within a period of two days from the declaration of default.

- Aggregation of the proprietary DMC‘s Position and the clients’ position that have not been ported. It will be possible the netting between the two positions. This means that long /short position of the DCM will be netted with the client’s short /long position where both of them were counterparties.

- Hedging of exposure to interest rate risk of the aggregated portfolio, by conducting open market transactions in the most liquid tenors of the rate curve or hedging buckets of liquid coverage.

- Auction of the aggregated position and corresponding hedging transactions among the NDCM. This position can be divided into manageable similar portfolios, either by number of operations or rate curve tenors, contained in that position, at the discretion of BME Clearing SWAPS advised by the GGI.

- Publication of the auction’s result by BME Clearing SWAPS. Thus may be resulting of a single or multiple winners. Likewise, the auction will be considered void for BME Clearing SWAPS if the price offered by the NDCM is not acceptable for the CCP.

- Total or partial position’s portability assigned in the auction to the account of the winner NDCM.

- Loss-sharing, if the case, incurred by auctioning the position of DCM.

The Defult Management Group (DMG) is the advisory and supporting committee of the CCP during the Default Process. This committee is composed of individuals from both the NDCM, with proven track record and market experience, and the CCP. Attendance to this group is mandatory.

The DMG functions are, among others:

- Organizations of the fire-drills.

- Set the guidelines of the auction.

- Proposal of improvements of the rules and procedures relating the default management.

- Proposal of the time and way to conduct the hedging transactions of the DCM’s position.

- Proposal of the DCM’s portfolio splitting, or if the case, the division into Auction Units.

- Proposal of the Auction Model, in terms of number of NDCM winners.

- Definition of the Schedule (dates and time) for the portfolio’s auction.

- And, in general any subject related to the default process that BME Clearing could ask for advice.

Once the CM has been declared in default and hedged, if necessary, his position, BME Clearing will proceed to auction the DCM’s position among the NDCM.

For this purpose the CCP, every time advised by the DMG, will decide previously whether or not split the DCM’s position (either by curve tenors or floating references, Euribor , Eonia, EuroSTR) and the auction model (if there is a single or several winners, in which case they will have to define Auction Units (AU) for each NDCM must bid).

Once decided, the NDCM shall communicate to the CCP the bid amount by position or assigned AU. The bid price is the NPV of the position for which the NDCM has to bid.

BME Clearing solves auction assigning the position at the best price. In case of two best prices were equal, CCP will use the temporary FIFO (first auction to arrive is the winner). The CCP may declare the auction null and void if the bid price does not reach a reasonable level under CCP’s criteria. Bids may be positive, when the NDCM has to pay BME CLEARING the price, or, on the other hand, negative, if the NDCM has to receive the bid price from BME Clearing. Shall be the duty of all the MCNI attend the auction with bids, although one NDCM may delegate in another NDCM this obligation.

Once resolved the auction, the winner NDCM will become the owner of the assigned position, with all rights and obligations. All liquidations corresponding to the auctioned position are the responsibility of DCM until it is registered in the name of the winner NDCM.

In the event that the auction of the position may incur losses, these will be absorbed into 3 levels:

- Level 1: All margins posted by the DCM (Initial margin, Individual Margin and his contribution to the Default Fund).

- Level 2: BME Clearing’s own resources in the swaps’ segment ("Skin in the game")

- Level 3: The contribution to Default Fund of NDCM according their CCP’s risk share.

If all these levels of defense were not enough, then will come into play BME Clearing’s own Resources, reaching, if the case, to close the business at the Swaps’ segment.

BME Clearing will carry out, along with CM, Fire Drills to replicate the event of a default.

The main objective for these FD is to make sure that not only the CCP but also the CM are ready to face the default of a CM and run all the Default Management Process accurately.

These FD will cover all the sides, from technical (Auction processing, portfolio’s splitting, client positions and accounts’ porting, etc.) to market (time and size of the hedging transactions, etc.)

The number of FD may vary from 1 to 3 in a year and attendance will be mandatory for all CM.

Detailed operation

The calendar for registration and settlement processes at BME Clearing SWAPS will be ruled by TARGET calendar.

Opening and closing hours of each process for a day are pointed in the chart below:

|

Time

|

Process

|

|---|---|

|

09:00

|

Start of Session Multilateral settlement. Opening of the transaction registration. |

|

12:00 |

Portfolio revaluation. |

|

15:00 |

Portfolio revaluation. |

|

18:00 |

End of Session Close of the transaction registration. |

|

21:00 |

Reports sending. |

The Clearing Member activity will be informed by BME Clearing through the files as follow:

- Intraday (ID): With a frequency no longer than 10 min, when the Clearing Member have activity to report.

- End of Day (EoD): Once the BME Clearing close its activity for the session date, will send the files.

The files will be obtain on EoD through the SFTP access of BME Clearing.

|

GROUP

|

FILE NAME

|

FILE CODE

|

DESCRIPCTION

|

FORMAT |

|---|---|---|---|---|

|

GENERAL DATA |

CFIXING |

REP-GENDAT-001 |

Informs the fixings rate by Index reference for the last 12 month, included the current session. Also spot exchange rate for currencies other than the setllement one.

|

CSV |

|

CCALENDAR

|

Row 2, Column REP-GENDAT-0023

|

Informs the non-working days, according to the Calendar specified by the eligibility criteria. |

CSV |

|

|

CCURVES |

REP-GENDAT-003 |

Informs the Zero Rates curves used and discount Factor. Also, it informs about the used rates for the curve building. |

CSV |

|

|

CLIQUIDITYMARGIN |

REP-GENDAT-004 |

Informs the parameterization for the size position adjustment. it must contain as many parameterizations as kind of generics used for the ATP and Liquid Margin. |

CSV |

|

|

|

CGENERICPRODUCTS |

REP-GENDAT-005 |

Informs about the generic products used for the LiquidityMargin calculations. For each generic, the kind of risk asociated must be identified. |

CSV |

|

|

CSCENARIOS |

REP-GENDAT-006 |

Informs all scenarios used for the margins calculations, included no VaR scaled scenario table. It also informs all hipotetical scenarios used for StressTest, included no VaR scaled scenario table. |

CSV |

|

TRADES |

CBACKLOADINGPREVISION |

REP-OP-001 |

Informs to Clearing Members and by Account level the Initial Margin and Variation Margin for all pending trades for the current Backloading process. If the Report destination Member is Clearing Member, the report shall include also the trades of other CCP members which are cleared by the Clearing Member. |

CSV |

|

|

CTRADES |

REP-OPIN-001 |

Informs the Clearing Member and by Account level all trades: received and novated by the CCP, new trades generated in the Post - Register Events as: Netting, Transfer, Modified non-economic data, Maturity trades, all events that apply over the trades and final trade status. This file does not contain all the economics trade details. If the Report destination Member is Clearing Member, the report shall include also the trades of other CCP members which are cleared by the Clearing Member. |

CSV |

|

OPEN POSITION |

COPINIRSFRA |

REP-OPIN-002 |

Informs the Clearing Member and by Account level all Swap`s and FRA`s live trades details and trade status. If the Report destination Member is Clearing Member, the report shall include also the trades of other CCP members which are cleared by the Clearing Member. |

CSV |

|

CCOUPONS |

REP-OPIN-003 |

Informs the Clearing Member and by Account level the details of the coupons amount for all fixed and stimate flows to receive/pay by trade. This report contain Swaps and Fras. If the Report destination Member is Clearing Member, the report shall include also the trades of other CCP members which are cleared by the Clearing Member. |

CSV |

|

|

|

CCONSIDERATIONS |

REP-OPIN-004 |

Informs the Clearing Member and by Account level the all future and past upfront flows to receive/pay by trade. If the Report destination Member is Clearing Member, the report shall include also the trades of other CCP members which are cleared by the Clearing Member. |

CSV |

|

|

CMARGINPARAMETERS |

REP-MAR-001 |

Informs the calculation Margin model.

|

CSV |

|

MARGINS |

CSENSITIVITY |

REP-MAR-002 |

Informs the Clearing Member and by Account level, the sensitivities variations in the interest rate. If the Report destination Member is Clearing Member, the report shall include also the accounts of other CCP members which are cleared by the Clearing Member. |

CSV |

|

CLIQUIDMARGIN |

REP-MAR-003 |

Informs the Clearing Members and by Account level, the hedge trades taken for the liquidity margin calculation. If the Report destination Member is Clearing Member, the report shall include also the accounts of other CCP members which are cleared by the Clearing Member. |

CSV |

|

|

CTOTALINITIALMARGIN |

REP-MAR-004 |

Informs the Clearing Member and by Account level, Total IM calculated today , current calculation method, current NPV, current VM, calculation method from d-1, Total IM from D-1, NPV from D-1, VM from D-1. If the Report destination Member is Clearing Member, the report shall include also other CCP members accounts which are cleared by the Clearing Member. |

CSV |

|

|

CSTRESSTESTING |

REP-MAR-005 |

Informs the Clearing Member and by Account level, the Stress test results. |

CSV |

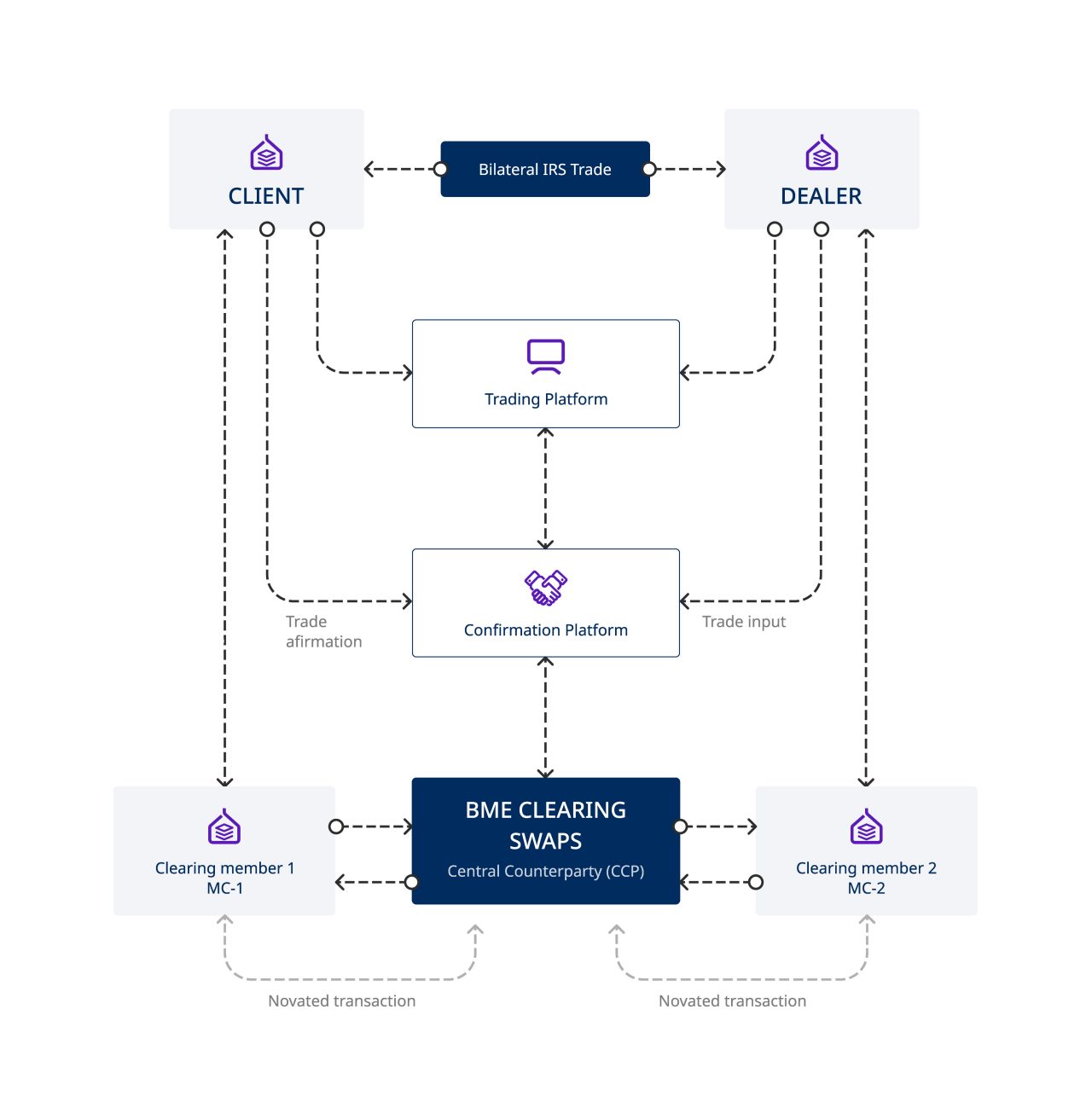

The CCP will provide services of liabilities compensation and the calculation, posting and management of margins.

The novation of the trade takes place at the time when the CCP registers the trades communicated trough a trade's affirmation platform.

An example of this clearing flow is shown below:

When transactions have been registered in the CCP, Members may undertake the following explicit actions, provided no term, condition or economic obligation is not changed by the Members, as defined below:

|

Post-Registration Events

|

Description

|

|

Result |

|---|---|---|---|

|

Netting

|

BME CLEARING BME CLEARING may net transactions according to the elegible criteria for netting in one of two ways: A.- at Transaction level: Members must state that they wish to carry out netting of their transactions and positions once they are registered in the clearing house. To do so, they must identify the Transaction to be netted with an ID number (NID). B.- at Account level: Transactions will only be nettable if they belong to the same Account and Sub-account: that is, transactions within the same Account cannot be netted if the transactions do not belong to the same sub-account. |

Partial |

Termination or Cancellation of original transactions |

|

Registration of new transaction for the remaining Notional |

|||

|

Totally |

Termination or Cancellation of original transactions |

||

|

Modification of non-economic data |

Refers modification of some trade economics details as below: a) Trade identifier of the Client. |

A new operation isn´t generated, the economic terms of the transaction are held. |

|

|

Cancellation of trades

|

All trades unwind parcial or totally, follow the netting process. |

Partial |

Termination or Cancellation of original transactions. |

|

Registration of new transaction for the remaining Notional. |

|||

|

Totally |

Termination or Cancellation of original transactions. |

||

|

Portability and Transfer of Trades |

Is the ability of a Clearing Member to transfer its position and collateral to another Clearing Member, without close-out or re-register. |

A new operation isn´t generated, the economic terms of the transaction are held. Account ans sub account will modified. |

|

Frequently asked questions

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Vivamus at auctor mauris. Nullam feugiat tempor neque, sed dignissim massa accumsan eget. Duis mauris magna, eleifend a mauris in, sagittis viverra felis. Curabitur ornare malesuada accumsan. Suspendisse sollicitudin diam nec pretium mattis. Proin porta lacus vel sem venenatis, ut egestas nunc maximus. Curabitur rutrum nibh pharetra enim faucibus mattis. Phasellus malesuada ligula non purus fringilla, quis sollicitudin sem tincidunt. Vestibulum lacus est, consequat ut risus vitae, tincidunt posuere nisi. Praesent nibh lacus, ullamcorper eget auctor vel, mattis at mauris. Proin sed elit justo. Nunc tempus sapien velit, at feugiat nisi bibendum eu. In at bibendum nisl, non posuere mi. Fusce tincidunt, ligula a consectetur sagittis, velit est feugiat nulla, eu vehicula sapien magna ut nunc.